With federal climate disclosure requirements facing uncertainty, U.S. states are accelerating their own regulatory action. Following California’s landmark climate laws, New York has now advanced the Corporate Climate Accountability Act (CCDAA) (Senate Bill S9072A). If your company generates more than $1 billion in annual revenue, this legislation will likely apply to you, and preparation should begin now.

What is New York’s Corporate Climate Accountability Act

New York’s Corporate Climate Accountability Act would require certain large companies doing business in the state to publicly disclose their greenhouse gas emissions each year. The goal is to create greater transparency and accountability around corporate climate impacts.

Covered companies would be required to report emissions across all three scopes:

Scope 1: Direct emissions from sources the company owns or controls

Scope 2: Indirect emissions from purchased electricity, steam, heating, or cooling

Scope 3: Indirect emissions across the value chain, including upstream and downstream activities not directly controlled by the company

By including Scope 3 emissions, the Act aims to provide a more complete picture of a company’s total climate impact- addressing gaps that have historically limited corporate disclosures.

Emissions would need to be calculated in accordance with Greenhouse Gas Protocol standards, ensuring alignment with globally accepted methodologies and improving comparability across companies and jurisdictions.

All reported data would be published on a centralized digital platform, making disclosures publicly accessible and allowing investors, regulators, and other stakeholders to review and compare corporate climate performance.

Where the Bill Stands

The CCDAA was introduced in January 2025 and passed by the New York State Senate on February 20, 2026. It now moves to the Assembly for consideration before heading to the Governor’s desk.

For companies that may fall within scope, waiting for final passage before acting would be risky. The timeline for implementation begins quickly.

Who’s in Scope?

The Act applies to:

U.S.-based public and private companies

With annual revenues exceeding $1 billion

Unlike New York’s existing greenhouse gas reporting program, which applies at the facility level, the CCDAA applies at the entity (company-wide) level.

This means corporate ESG, finance, and compliance teams, not just environmental managers at individual facilities, will need to own compliance.

What Companies Must Report

Beginning in 2027 (covering fiscal year 2026), companies must publicly disclose:

Scope 1 emissions

Scope 2 emissions

Scope 3 emissions

All emissions must be calculated in accordance with the Greenhouse Gas Protocol. For many companies, Scope 3 emissions will represent the largest portion of total footprint and the most complex to calculate.

Reports must be:

Publicly available

Easily accessible

Submitted annually

Assurance Requirements: What Changes Over Time

Verification is not optional.

The CCDAA phases in third-party assurance as follows:

Scope 1 & 2:

Limited assurance beginning in 2028

Reasonable assurance beginning in 2032

Scope 3:

The Department will evaluate assurance requirements in 2029

If required, limited assurance would begin in 2032

For sustainability teams, this means documentation quality, data traceability, and internal controls must be audit-ready, not just disclosure-ready.

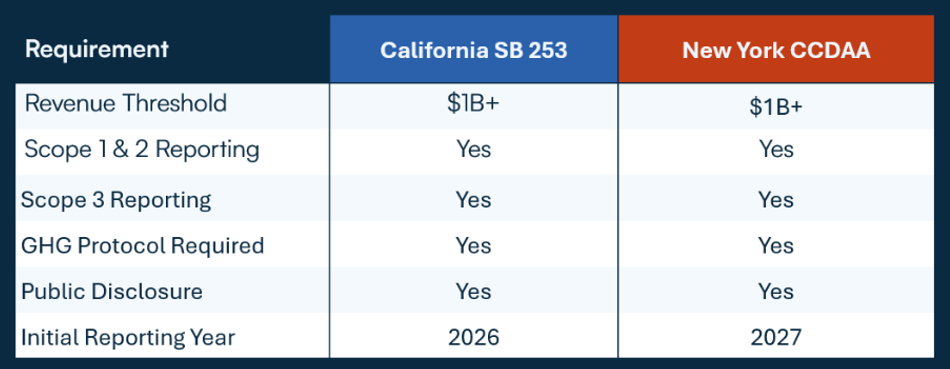

How It Compares to California’s SB 253

The CCDAA closely mirrors California’s SB 253 in structure and ambition:

For companies already preparing for SB 253 compliance, much of the groundwork (emissions inventories, data systems, Scope 3 screening) will support CCDAA compliance as well.

How This Differs from New York’s Existing GHG Reporting Program

New York already operates a greenhouse gas reporting program, but the purpose and scope differ significantly.

Existing NY Program:

Applies to facilities emitting over 10,000 tCO₂e

Facility-level reporting

Supports state-level emissions tracking

CCDAA:

Applies at the corporate level

Targets large corporations

Requires Scope 3 reporting

Focuses on public disclosure and investor transparency

This is not simply an expansion of existing environmental reporting; it is a corporate disclosure regime.

What ESG Teams Should Be Doing Now

If You Have Not Yet Conducted a Full Carbon Inventory

Define your organizational boundary (financial control vs. operational control).

Conduct a Scope 1, 2, and high-level Scope 3 screening assessment.

Identify data owners across procurement, finance, operations, and logistics.

Determine where primary data is feasible versus where estimates will be required.

Begin evaluating verification providers early.

Starting now allows you to test data quality before assurance becomes mandatory.

If You Already Have a Carbon Inventory

Review alignment with the Greenhouse Gas Protocol (including Scope 3 category completeness).

Strengthen documentation and internal controls in anticipation of assurance.

Conduct a gap assessment between current practices and limited assurance expectations.

Stress-test Scope 3 methodologies, particularly purchased goods and services, use of sold products, and transportation.

Companies that treat 2026 as a “dry run” year will be in a significantly stronger position than those rushing to comply in 2027.

How CEMAsys Supports CCDAA and SB 253 Compliance

CEMAsys supports organizations through the full carbon accounting lifecycle:

Organizational boundary definition

Scope 1-3 emissions calculation aligned with the Greenhouse Gas Protocol

Scope 3 relevance screening

Data collection system

Verification preparation and audit support

Year-over-year reporting optimization

Our GHG Accounting software eliminates the need for manual emission factor sourcing, increases traceability, and supports audit-ready documentation, helping sustainability teams build repeatable and defensible reporting processes.

For companies navigating multi-state climate disclosure requirements, having a structured system in place is no longer optional, it is a risk management necessity.

Final Takeaway

The New York Corporate Climate Accountability Act signals a clear trend: state-level climate disclosure requirements are expanding, not contracting.

For companies with over $1 billion in revenue, 2026 data collection is effectively the starting line.

Whether you are already preparing for SB 253 or just beginning your carbon accounting journey, now is the time to ensure your inventory is complete, defensible, and assurance ready.

If you would like to assess your organization’s readiness for CCDAA compliance, our team at CEMAsys is happy to connect.

Get access by filling in the form

Thank you for your interest - your file is now ready to download.

Oops! Something went wrong while submitting the form.

What is New York’s Corporate Climate Accountability Act

New York’s Corporate Climate Accountability Act would require certain large companies doing business in the state to publicly disclose their greenhouse gas emissions each year. The goal is to create greater transparency and accountability around corporate climate impacts.

Covered companies would be required to report emissions across all three scopes:

Scope 1: Direct emissions from sources the company owns or controls

Scope 2: Indirect emissions from purchased electricity, steam, heating, or cooling

Scope 3: Indirect emissions across the value chain, including upstream and downstream activities not directly controlled by the company

By including Scope 3 emissions, the Act aims to provide a more complete picture of a company’s total climate impact- addressing gaps that have historically limited corporate disclosures.

Emissions would need to be calculated in accordance with Greenhouse Gas Protocol standards, ensuring alignment with globally accepted methodologies and improving comparability across companies and jurisdictions.

All reported data would be published on a centralized digital platform, making disclosures publicly accessible and allowing investors, regulators, and other stakeholders to review and compare corporate climate performance.

Where the Bill Stands

The CCDAA was introduced in January 2025 and passed by the New York State Senate on February 20, 2026. It now moves to the Assembly for consideration before heading to the Governor’s desk.

For companies that may fall within scope, waiting for final passage before acting would be risky. The timeline for implementation begins quickly.

Who’s in Scope?

The Act applies to:

U.S.-based public and private companies

With annual revenues exceeding $1 billion

Unlike New York’s existing greenhouse gas reporting program, which applies at the facility level, the CCDAA applies at the entity (company-wide) level.

This means corporate ESG, finance, and compliance teams, not just environmental managers at individual facilities, will need to own compliance.

What Companies Must Report

Beginning in 2027 (covering fiscal year 2026), companies must publicly disclose:

Scope 1 emissions

Scope 2 emissions

Scope 3 emissions

All emissions must be calculated in accordance with the Greenhouse Gas Protocol. For many companies, Scope 3 emissions will represent the largest portion of total footprint and the most complex to calculate.

Reports must be:

Publicly available

Easily accessible

Submitted annually

Assurance Requirements: What Changes Over Time

Verification is not optional.

The CCDAA phases in third-party assurance as follows:

Scope 1 & 2:

Limited assurance beginning in 2028

Reasonable assurance beginning in 2032

Scope 3:

The Department will evaluate assurance requirements in 2029

If required, limited assurance would begin in 2032

For sustainability teams, this means documentation quality, data traceability, and internal controls must be audit-ready, not just disclosure-ready.

How It Compares to California’s SB 253

The CCDAA closely mirrors California’s SB 253 in structure and ambition:

For companies already preparing for SB 253 compliance, much of the groundwork (emissions inventories, data systems, Scope 3 screening) will support CCDAA compliance as well.

How This Differs from New York’s Existing GHG Reporting Program

New York already operates a greenhouse gas reporting program, but the purpose and scope differ significantly.

Existing NY Program:

Applies to facilities emitting over 10,000 tCO₂e

Facility-level reporting

Supports state-level emissions tracking

CCDAA:

Applies at the corporate level

Targets large corporations

Requires Scope 3 reporting

Focuses on public disclosure and investor transparency

This is not simply an expansion of existing environmental reporting; it is a corporate disclosure regime.

What ESG Teams Should Be Doing Now

If You Have Not Yet Conducted a Full Carbon Inventory

Define your organizational boundary (financial control vs. operational control).

Conduct a Scope 1, 2, and high-level Scope 3 screening assessment.

Identify data owners across procurement, finance, operations, and logistics.

Determine where primary data is feasible versus where estimates will be required.

Begin evaluating verification providers early.

Starting now allows you to test data quality before assurance becomes mandatory.

If You Already Have a Carbon Inventory

Review alignment with the Greenhouse Gas Protocol (including Scope 3 category completeness).

Strengthen documentation and internal controls in anticipation of assurance.

Conduct a gap assessment between current practices and limited assurance expectations.

Stress-test Scope 3 methodologies, particularly purchased goods and services, use of sold products, and transportation.

Companies that treat 2026 as a “dry run” year will be in a significantly stronger position than those rushing to comply in 2027.

How CEMAsys Supports CCDAA and SB 253 Compliance

CEMAsys supports organizations through the full carbon accounting lifecycle:

Organizational boundary definition

Scope 1-3 emissions calculation aligned with the Greenhouse Gas Protocol

Scope 3 relevance screening

Data collection system

Verification preparation and audit support

Year-over-year reporting optimization

Our GHG Accounting software eliminates the need for manual emission factor sourcing, increases traceability, and supports audit-ready documentation, helping sustainability teams build repeatable and defensible reporting processes.

For companies navigating multi-state climate disclosure requirements, having a structured system in place is no longer optional, it is a risk management necessity.

Final Takeaway

The New York Corporate Climate Accountability Act signals a clear trend: state-level climate disclosure requirements are expanding, not contracting.

For companies with over $1 billion in revenue, 2026 data collection is effectively the starting line.

Whether you are already preparing for SB 253 or just beginning your carbon accounting journey, now is the time to ensure your inventory is complete, defensible, and assurance ready.

If you would like to assess your organization’s readiness for CCDAA compliance, our team at CEMAsys is happy to connect.

Emily is a sustainability and ESG consultant who partners with organizations to align climate ambition with regulatory and disclosure requirements. She specializes in environmental compliance, CDP reporting, and science-based target setting (SBTi), helping clients simplify complex reporting obligations while advancing credible, high-impact climate strategies.

By clicking "Accept cookies", you consent to cookies being stored on your device to enhance site navigation, analyze site usage, and assist in our marketing efforts. See our privacy policy.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.avif)